The Role of Credit Cards in Building Customer Relationships

In our previous blog “The Credit Card Issuing Opportunity for Community Banks,” we highlighted the considerable opportunity for banks to improve their services and participate in the lucrative credit card issuing market. Now, we will discuss the next steps to this process, focusing on profitable business relationship customers.

A recent FDIC study of community banks revealed that small businesses and middle market companies more frequently turn to banks for credit, particularly if the business owner has a relationship with a lender. Currently, community banks successfully provide 44% of small business financing, yet they capture almost 0% of credit card loans4.

Small businesses, municipalities and non-profits want to get financial products from their local bank, but most community banks do not offer relationship-based credit cards to their business customers other than through a referral program to an Agent Bank. Many small business owners choose to bank their personal and business finances at the same local bank. According to BAI research, community banks and credit unions have the lowest NPS (Net Promoter Score) from business owners8. Offering business credit cards presents an excellent opportunity to strengthen customer relationships and provide additional value.

Insights from Industry Surveys: Business Credit Cards

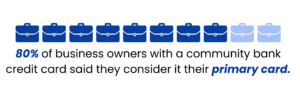

In a survey by AT Kearney & Visa, small businesses revealed their likelihood of getting a business card in the next two years. The results showed that 69% of businesses said they are somewhat likely and 38% are likely5. In the same survey, 40% of the business customers with a community bank relationship said they would consider them for a business credit card if one was offered to them, and 80% of businesses with a community bank card said they consider it their primary card5.

CorServ has found that businesses are the single most important element to our bank client’s success in credit card profitability. Dozens of CorServ bank clients report that businesses make up 80% of their credit card loans and even more of their credit card profits.

The Benefits of Business Credit Cards

Business credit cards are profitable for banks through interchange fees, interest and other fees similar to a personal credit card. By issuing business credit cards, banks provide businesses with a convenient way to review transactions, track expenses and earn rewards. Providing convenient financial tools for customers will strengthen the business relationship and help retain long-lasting customers that will utilize additional financial products.

CorServ Features and Services

When companies start a credit card program with one of CorServ’s partner banks, they have access to their turnkey, brandable, browser-based interface for business administrators. It provides the self-service features that companies want, and it is optimized for viewing on computers, tablets and mobile phones. It can be branded with your company logos, colors, payment card images, splash screens and marketing messages. In addition, companies can utilize CorServ’s expense reporting system to enhance the value of the payment card solutions.

It is critical for banks to leverage business customer relationships. These customers with deep relationships across bank products are among the most profitable customers for banks. Small businesses are indicating their interest in business credit cards, and banks must capitalize on this opportunity through business customers. By adopting a strategic approach to business credit cards, community banks can significantly enhance their service offerings, strengthen business customer relationships, and drive profitability.

Download the full guide or contact CorServ for more information about starting a credit card program.

Sources

- Reinventing credit cards: Responses to new lending models in the US, McKinsey and Company.

- FDIC Call Reports

- Nielson Report: Top Issuers of General Purpose Credit Cards in the US

- FDIC Community Banking Study: Notable Lending Strengths of Community Banks

- Small Business Credit Cards: How Banks Can Harness the Opportunity – Visa and ATKearney

- Credit Card portfolio for CorServ bank partners average ROA from 2021-2023

- Commercial Pay Payments Industry Insights – MasterCard and Mercator Advisory Group

- BIA Research March 2024: Small Business Banking Trends