Understanding the Credit Card Issuing Opportunity

Credit cards have consistently stood out as one of the most profitable products for banks in the United States, typically yielding a return on assets (ROA) ranging from 3% to 4% (1). This financial success stems from a combination of revenue streams, including interchange rates, interest, and various fees. However, these earnings are offset by expenses such as reward redemptions, cost-of-funds, credit and fraud losses, and operating expenses. The average ROA across all U.S banks stands at about 1% (2). In comparison, relationship-based credit cards can outperform this average, potentially generating an ROA of up to 6% for financial institutions (6).

Current Market Trends

In 2022, the 10 largest credit card issuers collectively recorded $4.492 trillion in purchase volume, dominating the market with an 82.4% share (3). By the fourth quarter of 2023, consumer credit card balances had surged to $1.13 trillion, marking a $50 billion increase in just one quarter (3). These patterns suggest an expansion in market size in the coming years, driven by the rising demand for consumer credit cards and the increasing volume of small business and commercial credit cards.

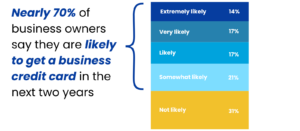

Business owners want business credit cards from their bank in the next two years.

Why Banks Are Missing Out on This Opportunity

In the U.S., there are over 4,500 banks, but only 1% of these banks own 99% of credit card loans (2). For over 70 years, most U.S. banks have not effectively participated in the high-margin credit card issuing business, despite it being one of the best-performing financial products. Banks not capitalizing on the credit card issuing opportunity are letting their relationship customers obtain credit card services from other banks.

Today, technology and end-to-end Program Management is now available for all U.S. banks to launch and own credit card programs in 120 days or less. CorServ’s technologies and services encompass every aspect of credit card disciplines, including origination, credit decision making, processing, sales/servicing interfaces, detailed reporting, integrated rewards, marketing, compliance support, and risk management.

The Way Forward

It is essential for banks across the U.S. to understand the credit card issuing opportunity that allows them to capitalize on one of the best-performing financial products and potentially yield an ROA from 3% to 4%. Innovative payment card issuing companies like CorServ present a significant opportunity for banks to enhance their offerings and capture a share of the lucrative credit card issuing business.

Embracing these advancements and leveraging comprehensive program management solutions will enable more banks to enter the credit card market effectively. By doing so, banks can secure higher profitability and strengthen their customer relationships in the competitive financial landscape.

To learn more about the steps you can take to be successful in the high margin credit card issuing market, download the full white paper or contact CorServ for more information about starting a credit card program.

Sources

1. Reinventing credit cards: Responses to new lending models in the US, McKinsey and Company.

2. FDIC Call Reports

3. Nielson Report: Top Issuers of General Purpose Credit Cards in the US

4. FDIC Community Banking Study: Notable Lending Strengths of Community Banks

5. Small Business Credit Cards: How Banks Can Harness the Opportunity – Visa and ATKearney

6. Credit Card portfolio for CorServ bank partners average ROA from 2021-2023

7. Commercial Pay Payments Industry Insights –MasterCard and Mercator Advisory Group