By executing 5 simple steps, US banks have an opportunity to participate in the high margin credit card issuing business which most are missing today.

- Understand the Credit Card Issuing Opportunity

- Leverage Business Relationship Customers

- Find a Credit Card Program that your Bank Owns

- Focus on Commercial Credit Cards

- Promote a Sales Culture for Credit Cards

Understand the Credit Card Issuing Opportunity

Credit cards in the US have historically been one of the highest margin products for banks, averaging 3%-4% Return on Assets (ROA). Credit card issuing banks earn income from interchange, interest, and fees.

Expenses include reward redemptions, cost-of-funds, credit and fraud losses, and operating expenses. ROA is revenue minus expense. The average ROA for all products in U.S. banks averages about 1%. In comparison, relationship-based credit cards can generate ROA in excess of 6% for a financial institution.

In the United States, credit cards are one of the best-performing products in financial services, with a return on assets averaging 3%-4%.

The 10 largest issuers generated $4.492 trillion in purchase volume, giving them an 82.39% market share in 2022. Meanwhile, demand for credit cards continue to increase. Consumer credit card balances reached $1.13 trillion in the fourth quarter of 2023, increasing by $50 billion in a quarter. In addition, small business credit card and commercial credit card volumes are growing even faster.

There are still over 4,500 banks in the US, yet 1% of these banks own 99% of credit card loans.

Why is this?

For over 70 years, most US banks have not effectively participated in the high margin credit card issuing business. These banks are missing out on one of the best performing financial products, and letting their relationship customers get their credit card products from other banks. Technology and end-to-end program management is now available for all US banks to launch and own credit card programs in 120 days or less. Technology and services credit card disciplines include origination, credit decision making, processing, sales/servicing interfaces, detailed reporting, integrated rewards, market-ing, compliance support and risk management.

Leverage Business Relationship Customers

According to a recent FDIC study of community banks, in contrast to large corporations, which may be more likely to turn to the capital markets, small businesses (and middle market companies) more frequently turn to banks for credit, particularly if the business owner has a relationship with a lender.

Community banks successfully provide about 44% of small business financing, yet nearly 0% of credit card loans.

Banks provide approximately 44% of small business financing including all C&I loans and all non-farm, nonresidential loans. Small businesses, municipalities, and non-profits want to get financial products and services from their local bank.

But the vast majority of community banks do not offer relationship-based credit cards to their business community. Clearly, business customers with deeper relationships across bank products are among the most profitable customers for banks.

The opportunity is real

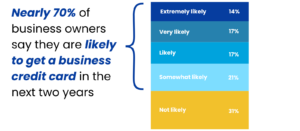

In a survey by AT Kearney & Visa, 69% of businesses said they are somewhat likely to get a new business credit card in the next two years, and 38% are likely. Businesses are looking for credit cards.

In the same survey, 48% of the businesses with a community bank relationship said they would consider them for a business credit card if one was offered to them…

…and 80% of businesses with a community bank card said they consider it their primary credit card.

Find a Credit Card Program that your Bank Owns

Typical Agent Bank Programs

Most banks are either not offering a credit card product, or more likely referring their customers to another bank running an Agent Bank program. In these programs, the referring bank gets a very small referral fee for credit card applications, and sometimes a small portion of Interchange, but they are losing their relationship customers to another bank for credit cards. The client banks have no say in the credit decision unless they guarantee any credit losses while not getting the interchange, interest, and fees from the cards.

In Agent Bank Programs, your bank only gets a small referral fee, and no say in the credit decision for your customers.

An option is for a bank to go direct to a credit card issuer processor where they do own the P&L and credit decisions. The challenge with this is that most banks don’t have the scale, expertise, or technology to successfully choose this option. For example, they will be required to provide their own underwriting technology and expertise, fraud prevention, and compliance. It is also more expensive with complicated line-item pricing and a 9-12 month implementation time.

CorServ’s Turnkey Program

A relatively new option in the past 10 years is CorServ’s turnkey credit card issuing program that enables client banks to launch within 120 days, offer their own branded credit cards to their businesses and consumers, and own the P&L for the program.

Client Banks own the interchange, loan interest, and fee income while a partnership with an Issuing Bank provides network sponsorship, compliance lead, and servicing functions.

Banks average over 6% ROA in CorServ’s program without investment in staff or infrastructure.

Client Banks recommend decisions for applications that do not reach an automated approval decision and have transparent access to detailed program data, reporting, and a servicing portal.

Focus on Commercial Credit Cards

Commercial credit card spend is gradually projected to increase in every product category, with total spend by mid-market companies at $590B in 2021.

Banks that want to stay competitive to retain medium to large commercial clients, including non-profits and local municipalities can recognize huge advantages from commercial credit cards. Commercial credit cards are becoming a crucial instrument for such companies. The 30-day float helps to manage cash flow. Employee expenses can be better managed and automated using the cards. Increasingly virtual cards with ePayables support are used to more efficiently pay vendors than checks or ACH.

Commercial card benefits include:

- Leverage for buyers: With the ability to float working capital from statement to statement, businesses can derive more value. The immediate reduction in the need for other financing results in lower interest costs and optimized capital use.

- Relief for suppliers: The relative cost, ease, and speed for suppliers to accept virtual cards is estimated to save 76% in cost and 72% in time versus a traditional purchase order process.

- Security from virtual cards: Virtual cards are a game-changer. These digital cards come with controls on amount, merchant, time frame and usage that reduce fraud. They include digital invoice data and offer a safer, more adaptable and more efficient way to handle B2B payments.

Middle Market virtual card spending is expected to grow by 332% over the next 3 years, faster than any other market segment according to MasterCard.

To start, find a program from a respected partner that:

- Let’s you own the interchange

- Can help you scale your program

- Supports Virtual Cards for ePayables

- Provides physical cards and expense reporting

- Includes a self-service portal for companies with spend controls

- Automates rebates you choose to give companies

- Provides reporting and analytics for your bank & companies

Promote a Sales Culture for Credit Cards

There is a huge market for credit cards, but your bank needs to embrace a sales culture that promotes the cards. In a new program where you own the P&L and can realize over 6% ROA, you will be more motivated to promote versus the Agent Bank program many banks now have. Focus on your relationship customer to reduce fraud and credit losses. Incorporate relationship data that is a key competitive advantage into your underwriting process.

Relationship credit card programs see much lower credit and fraud losses than national card programs and higher response to marketing offers.

Start with the most profitable commercial cards that can have a 13% ROA. Focus next on business cards and consumer cards that address market needs through several products, from a low rate (Prime + 2.99%) to a rich rewards card for high spenders. Offer long-term relationship products that keep APRs low and don’t have penalty rates.

Here are some best practices to establish a successful sales culture for credit cards:

- Automatically provide a commercial card with a line of credit to companies

- Sell on features like reduced cost and time to pay suppliers and process expenses before offering a rebate

- Organize branch sales contests or employee incentives, but train, track, and analyze sales to ensure compliance

- Data mine to determine relationship customers paying balances on competitors’ cards, and offer your card

Find a vendor where you own the P&L without investing in staff or infrastructure. You can realize over 6% ROA, and even higher on commercial cards.

Follow these 5 steps to create a successful credit card program with your relationship customers and enjoy the high-yielding assets of credit card loans on your balance sheet.

Sources

- Reinventing credit cards: Responses to new lending models in the US, McKinsey and Company.

- FDIC Call Reports

- Nielson Report: Top Issuers of General Purpose Credit Cards in the US

- FDIC Community Banking Study: Notable Lending Strengths of Community Banks

- Small Business Credit Cards: How Banks Can Harness the Opportunity – Visa and ATKearney

- Credit Card portfolio for CorServ bank partners average ROA from 2021-2023

- Commercial Pay Payments Industry Insights – MasterCard and Mercator Advisory Group